Showing posts with label housing. Show all posts

Showing posts with label housing. Show all posts

Tuesday, August 05, 2008

Costly gasoline hurts exurban house prices

The big lot and spacious house doesn't seem so great when you have to drive your 12 mpg Denali 45 miles each way to work. The Washington Post has some great graphics showing how housing prices in the core of DC have increased while the housing crisis is gutting exurban prices by 26% in the past year.

Tuesday, July 15, 2008

Mortgage crisis: Fannie, Freddie, and the rest

If you're familiar with "when banks compete, you win," then you probably listen to a news source that discusses the mortgage crisis. Paul Krugman's been keeping me informed, and he does a nice job of explaining what's going on:

- Fannie and Freddie are more closely regulated than private companies, so they're shenanigans were limited. They couldn't do subprime loans - loans given with no income verification - by rule.

- However, they weren't completely innocent, as they tried to stretch their ability to participate within the rules as much as possible.

- The housing market is so bad, that even these more regulated companies are sinking as people with conventional mortgages end up with negative equity.

Tuesday, December 11, 2007

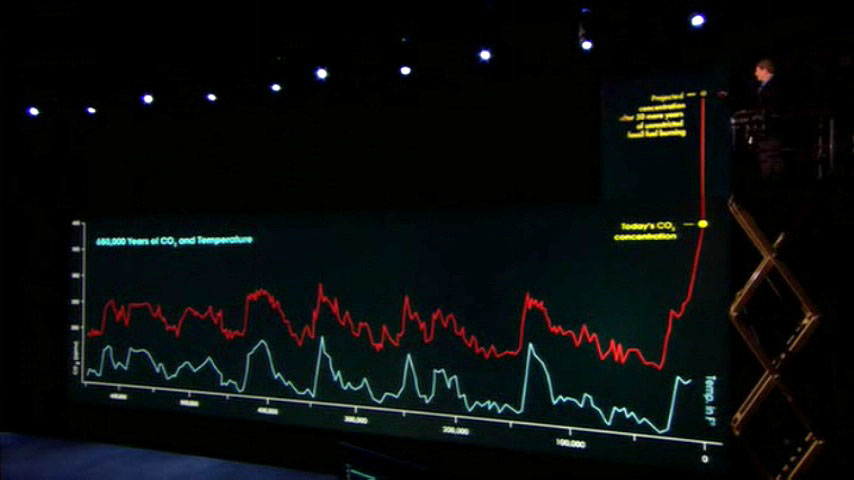

The housing bubble reminds me of An Inconvenient Truth

Basically, if housing prices get too high, people shouldn't be buying houses because renting will be cheaper. The linked chart shows the ratio of housing prices to rental prices, a measure of the imbalance in the residential market. The tail end we're on reminds me of the global carbon increase chart that Al Gore required a hydraulic lift to illustrate. This bubble hasn't begun to burst.

{kind=link}

Thursday, September 06, 2007

How home buying turned into the stock market

This is an interesting look at the way the mortgage market changed from a tightly regulated way to ensure homeowners had the income to buy a house to a quick way to make a buck.

In the golden age of American home buying — the years after World War II — savings-and-loan institutions or government agencies supplied returning G.I.’s with fixed 30-year mortgages. Home prices appreciated, steadily but at modest rates, and lending fiascoes were rare...The game continued, with non-bank entrants into the mortgage market offering all sorts of products like adjustable-rate mortgages or allowing people much more house than they could afford.

...The world began to change in the late 1970s, when Salomon Brothers...pioneered the mortgage security...Instead of keeping his mortgages in a drawer, the banker on Main Street could unload his risk by selling them to Salomon. The banker was thus converted from a long-term lender to a mere originator of loans.

Lenders and borrowers alike knew that such loans were dicey; they were counting on the borrowers to refinance — which, as long as home prices kept rising, was a cinch. Naturally, when prices stopped rising, the music stopped.So what happens now? Some states are looking to help bail out the unfortunate borrowers who didn't understand how their mortgage was merely a risky investment by a Wall Street hedge fund investor. But how to do so without rewarding the investor, who ought to be left holding the tab for their poor choice.

Wednesday, March 28, 2007

Houses are homes, not investments

While you're still better off building equity instead of paying rent (and deducting mortgage interest from your taxes), my friend at 28th Avenue notes that the housing market isn't the greatest right now.

The big thing: don't expect a lot of value appreciation in your home in the next couple years. 28th links to Calculated Risk, which quotes Fed Chair Bernanke:

The big thing: don't expect a lot of value appreciation in your home in the next couple years. 28th links to Calculated Risk, which quotes Fed Chair Bernanke:

To the downside, the correction in the housing market could turn out to be more severe than we currently expect, perhaps exacerbated by problems in the subprime sector. Moreover, we could yet see greater spillover from the weakness in housing to employment and consumer spending than has occurred thus far.Update 4/12: Check out the comments from EKM, where he links to an amazing tool posted by the New York Times for calculating whether it's better to rent or buy in your particular area.

Subscribe to:

Posts (Atom)